The Anatomy of Asia's 2026 Supply Chain Disruption

06/07/2026

In June, container vessels calling at the Port of Singapore faced berth waiting times of up to seven days, while the average dwell time for import containers surged from 2.9 to 9.2 days. What is happening at the world's largest container transshipment hub? Behind these figures lies a broader restructuring of global shipping networks, one that is sending ripple effects across Asian supply chains—from Singapore to Vietnam.

From Global Disruptions to Regional Network Reconfiguration

The latest disruptions affecting container shipping extend well beyond individual trade lanes.

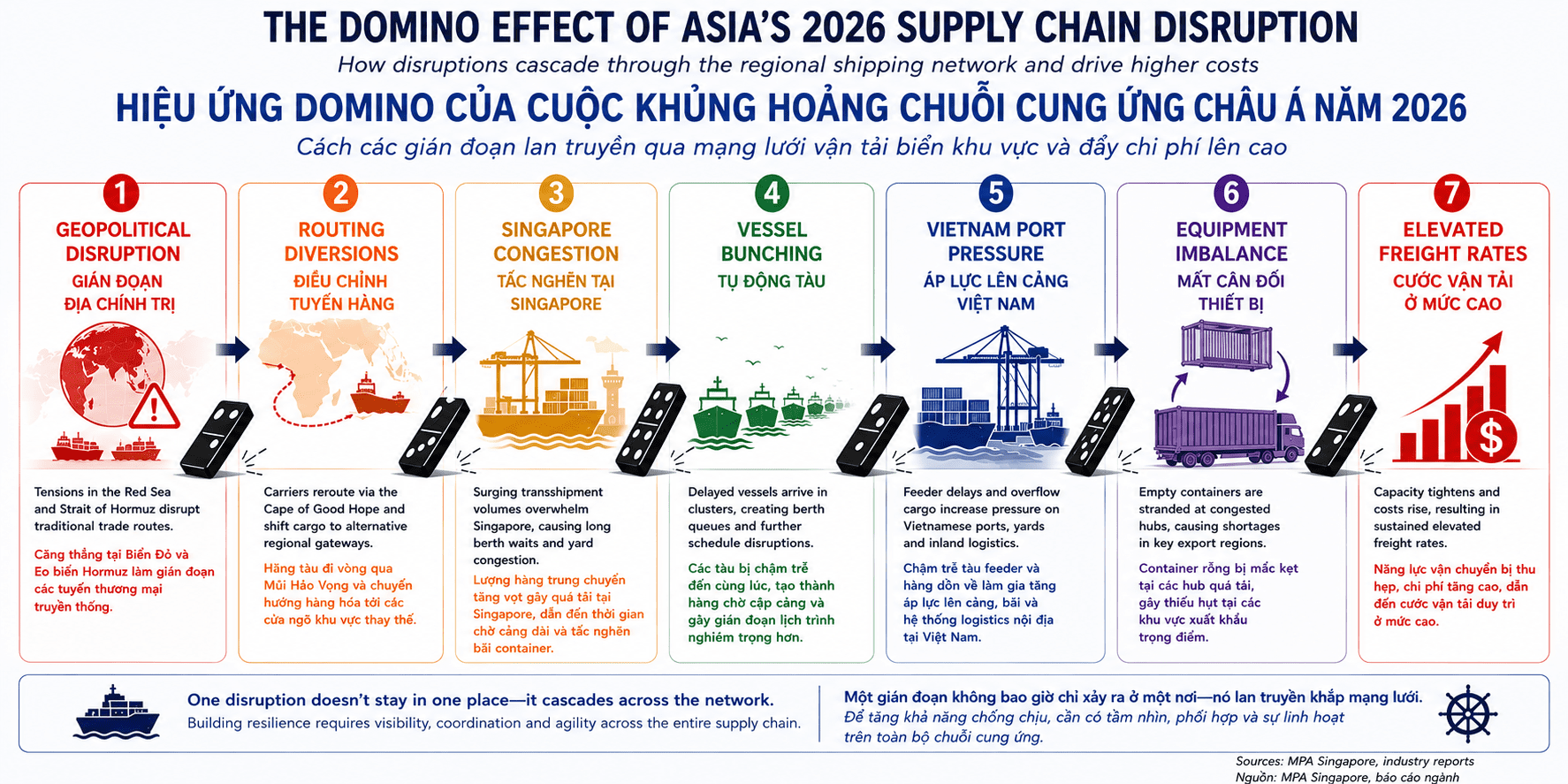

Security concerns in the Red Sea and around the Strait of Hormuz have forced carriers to redesign service networks, extend voyage distances, and adjust port rotations across Asia. Sailing around the Cape of Good Hope has added between 10 and 20 days to many long-haul services, effectively reducing available vessel capacity while increasing bunker consumption and schedule uncertainty.

Rather than maintaining traditional hub-and-spoke networks, many shipping lines have begun repositioning cargo through alternative regional gateways, particularly across the Indian Subcontinent and Southeast Asia. This has fundamentally altered cargo flows throughout the region.

The consequences are increasingly being felt not only at sea, but across the ports and inland logistics systems that support global supply chains.

Singapore: When the Region's Largest Transshipment Hub Reaches Saturation

Singapore illustrates how rapidly operational pressure can accumulate within a global hub.

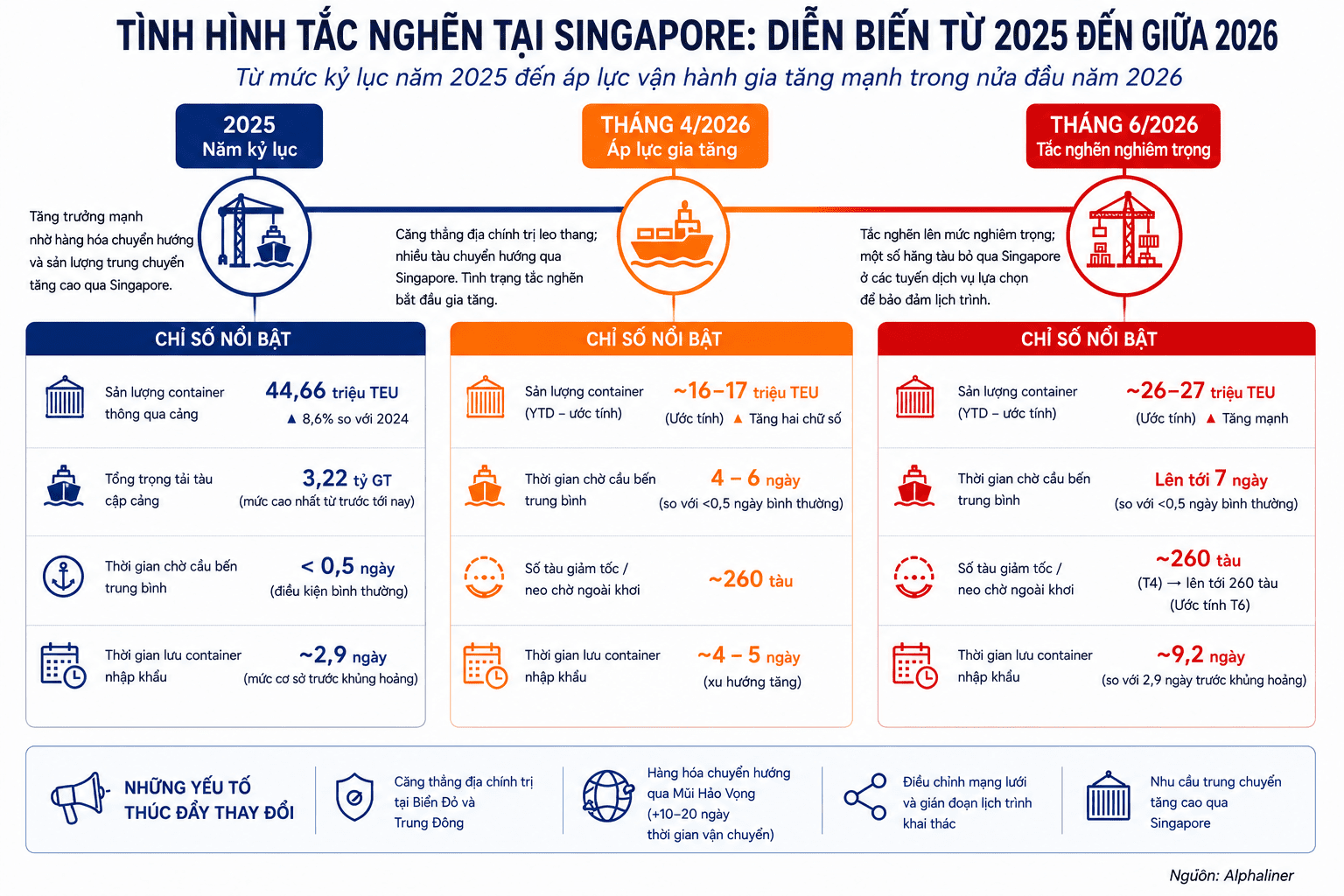

In 2025, the Port of Singapore handled a record 44.66 million TEUs, an increase of 8.6% over the previous year, while total vessel arrival tonnage reached an all-time high of 3.22 billion gross tons. The additional volume was largely driven by carriers rerouting cargo away from the Red Sea and Middle East corridors and consolidating transshipment activities through Singapore.

While these figures reflected the port's operational strength, they also meant that Singapore entered 2026 with very limited spare yard capacity.

As geopolitical tensions intensified during the first half of 2026, that operational buffer quickly disappeared.

By early April, average vessel waiting times had increased from less than half a day under normal conditions to between 4 and 6 days, while approximately 260 vessels were reported to be slow steaming or waiting offshore to align with delayed berth availability.

Conditions deteriorated further in June.

Waiting times reached as much as 7 days, with an estimated 450,000 TEUs queued within the port system awaiting berth access. Import container dwell time rose from 2.9 days before the crisis to 9.2 days, according to Alphaliner. Faced with prolonged delays, several major carriers began omitting Singapore from selected service rotations, discharging cargo at downstream ports or revising network loops instead.

Congestion Is Contagious

Congestion Is Contagious

Modern liner shipping operates as an interconnected network rather than a collection of individual ports.

Congestion at one major transshipment hub rapidly propagates through feeder services, inland logistics, container repositioning, and vessel schedules across the region.

When vessels are delayed at Singapore, they seldom recover their original schedules immediately. Instead, ships often arrive at subsequent ports in clusters—a phenomenon known as vessel bunching. Rather than receiving vessels at regular intervals, terminals must suddenly accommodate multiple large ships within a compressed timeframe.

This creates a cascading operational cycle:

- Yard occupancy rises rapidly.

- Truck arrivals become concentrated within shorter time windows.

- Container evacuation slows.

- Berth productivity declines.

- Subsequent vessels wait longer at anchorage.

- Schedule reliability deteriorates across entire service networks.

Under these conditions, congestion becomes increasingly self-reinforcing rather than self-correcting.

Vietnam: From Alternative Gateway to Regional Pressure Point

Vietnam: From Alternative Gateway to Regional Pressure Point

Vietnam has become one of the principal beneficiaries of changing regional shipping patterns, while simultaneously experiencing many of the operational pressures associated with higher cargo volumes.

During 2025, carriers increasingly favored direct calls at deep-water ports such as Cai Mep–Thi Vai and Lach Huyen as shippers sought to reduce dependence on congested transshipment hubs. National container throughput reached approximately 34 million TEUs, while vessel calls increased by 32% year-on-year.

The trend accelerated in early 2026.

Container throughput across Vietnam's seaport system reached 6.8 million TEUs during the first quarter, representing year-on-year growth of 12.1%. At the same time, growing operational pressure contributed to a 30% increase in median demurrage penalties, reflecting longer gate processing times and localized documentation delays in several southern logistics corridors.

By the end of May, cumulative container throughput had reached 15 million TEUs, up 14% compared with the same period in 2025. In response to rising operational pressure, the Vietnam Maritime and Inland Waterways Administration instructed port authorities to streamline administrative procedures and accelerate cargo release processes in an effort to maintain cargo flow.

Equipment Imbalances Extend Beyond the Port

Congestion affects more than vessels.

As containers remain longer inside port yards, the repositioning of empty equipment slows significantly.

The omission of Singapore from selected carrier rotations, together with longer feeder transit times, has complicated the redistribution of empty containers throughout Southeast Asia. Export-oriented markets—including Vietnam—face increasing challenges in securing equipment at the right locations and the right time, despite sufficient overall fleet capacity.

This illustrates an important distinction.

The current challenge is less about a shortage of ships than about the declining efficiency with which ships, containers, terminals, and inland transport networks are connected.

Operational Adaptation Becomes the New Competitive Advantage

The current disruption has reinforced a broader industry trend: operational resilience increasingly depends on network integration rather than individual asset capacity.

Port operators are placing greater emphasis on dynamic berth planning, yard optimization, and closer coordination with inland logistics facilities. Shipping lines continue to adjust service rotations, while cargo owners are extending booking windows and diversifying transport options through sea–air services, rail corridors, and alternative sourcing strategies.

Across Asia, the ability to coordinate ports, ICDs, depots, trucking fleets, and customs processes is becoming just as important as expanding physical infrastructure.

Market Outlook

The developments observed across Asia during 2026 suggest that freight rates are only one visible consequence of a broader structural adjustment taking place throughout regional supply chains.

Persistent congestion at major transshipment hubs, longer sailing distances, equipment imbalances, and evolving carrier network strategies continue to limit effective transport capacity despite ongoing fleet expansion.

For shippers and logistics providers, the priority is shifting from minimizing freight costs toward improving supply chain resilience. As regional cargo flows continue to evolve, operational agility and integrated logistics networks are likely to become the defining competitive advantages for ports and supply chain operators across Asia.