Opportunities, Growth Trends of Vietnam Seafood Industry

13/05/2026

Vietnam’s seafood industry entered 2026 on the back of growth momentum from 2025, when the sector’s total export value reached a record USD 11.3 billion, up 12.4% year on year. Alongside these positive developments, the seafood industry continues to face challenges arising from global political developments and supply chain disruptions.

Seafood Industry Challenges

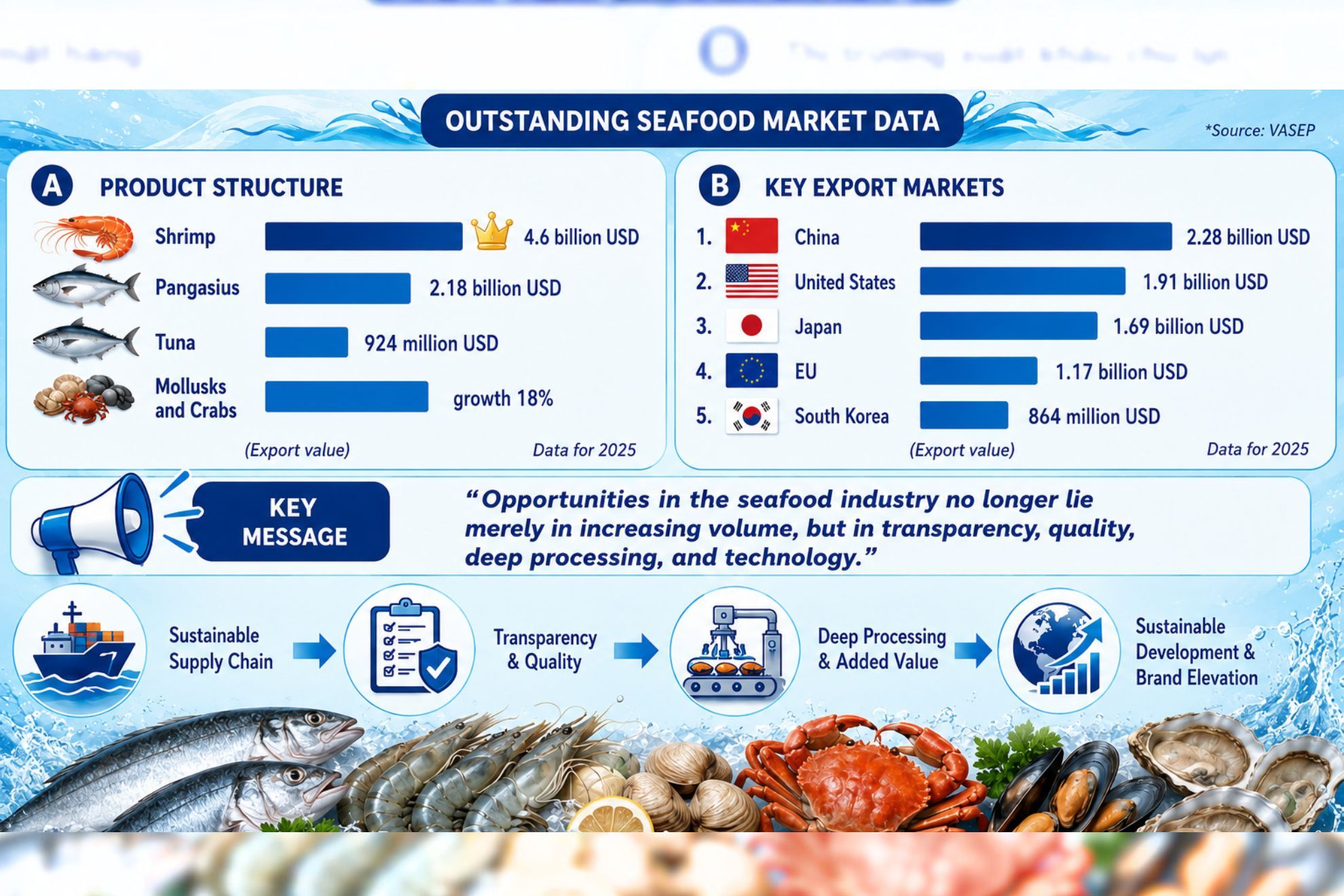

In terms of product structure, shrimp continued to play a leading role with USD 4.6 billion, pangasius reached USD 2.18 billion, tuna recorded USD 924 million, while the mollusk, crab and swimming crab group posted growth of 18%. By market, China rose to the top position with USD 2.28 billion, followed by the United States with USD 1.91 billion, Japan with USD 1.69 billion, the EU with USD 1.17 billion and South Korea with USD 864 million.

In terms of product structure, shrimp continued to play a leading role with USD 4.6 billion, pangasius reached USD 2.18 billion, tuna recorded USD 924 million, while the mollusk, crab and swimming crab group posted growth of 18%. By market, China rose to the top position with USD 2.28 billion, followed by the United States with USD 1.91 billion, Japan with USD 1.69 billion, the EU with USD 1.17 billion and South Korea with USD 864 million.

Overview of Vietnam Seafood industry in 2026

Overview of Vietnam Seafood industry in 2026In 2026, the seafood industry continued to record several positive signals. According to data announced by VASEP, seafood exports in March 2026 reached approximately USD 927 million, up more than 5% year on year; cumulative exports in the first quarter reached USD 2.64 billion, up nearly 8%. China and Hong Kong remained the strongest growth drivers, reaching around USD 764 million in the first quarter, up nearly 45%; in March alone, the figure exceeded USD 250 million, up over 50%. In practice, the seafood industry still faces a number of challenges as follows:

- Irregular order frequency: In reality, seafood exporters have yet to secure stable orders with regular frequency. In addition, profit margins have declined compared with the past. Exporters, shipping lines and ports therefore need to shift to a rolling weekly forecasting model, maintaining flexible cold-chain capacity and booking arrangements instead of locking monthly plans as in periods of stable demand.

- Declining profit margins: Amid continued global political and economic uncertainty, logistics costs, fuel costs, cold storage power costs and other operating expenses continue to increase, reducing the efficiency of export orders. As profit buffers become increasingly narrow, just a few additional days of yard storage, one empty container repositioning move, or an increase in reefer power costs can quickly erode the commercial efficiency of a shipment.

- Increasing compliance pressure: In addition to familiar requirements relating to quarantine, customs and food safety, enterprises must also meet increasingly stringent standards from importing markets. For the U.S. market, NOAA Fisheries requires a COA for shipments with COO+HTS combinations subject to restrictions under the MMPA, significantly increasing compliance risks for wild-caught seafood products. At the food supply chain level, although the FDA has not yet enforced the Food Traceability Rule before July 20, 2028, enterprises still need to proactively prepare CTE/KDE data and traceability plans. This shows that the enforcement timeline may be extended, but requirements for data standardization, information transparency and traceability across the supply chain have not been reduced.

Market Opportunities

From a market perspective, opportunities for the seafood industry remain present, but they no longer lie simply in increasing volume. The three important growth directions today include:

From a market perspective, opportunities for the seafood industry remain present, but they no longer lie simply in increasing volume. The three important growth directions today include:

- The global supply chain shift and long-term stable demand from importing markets.

- Increasing requirements from buyers for information transparency. Correspondingly, the industry is undergoing a value shift from price-based competition to quality-based competition.

- A transition from individual shipments to transparent traceability; from raw material exports to a higher proportion of deeply processed products and technology application.

Seafood industry opportunities

These trends are aligned with the requirements of major markets and represent a necessary direction for enterprises to improve profit margins amid rising compliance and operating costs.

From this reality, the seafood industry in 2026 is no longer only about “selling products”; it is about reorganizing the supply chain process to make it shorter, colder, faster and more transparent. This includes using diverse and flexible inland transport modes; developing cold-chain logistics centers; forming logistics clusters near raw material areas; building dedicated solutions for large-scale reefer cargo shipments; and continuing to optimize customs clearance procedures. If these links are implemented in a synchronized manner, the seafood industry can significantly reduce intermediary costs, shorten lead time and strengthen its competitiveness in both key markets and emerging markets.

Overall, Vietnam’s seafood industry is moving through a pivotal stage: growth remains, but it is no longer easy; opportunities remain open, but they require a higher level of supply chain organization. In the context of first-quarter 2026 exports increasing by nearly 8% and China continuing to play a leading market role, what matters for enterprises is not only capturing short-term demand momentum, but also investing in a more sustainable export structure based on cargo quality, cold-chain logistics, traceability and the ability to respond quickly to market fluctuations. This is also the pathway for Vietnam’s seafood industry to move from the position of a “strong exporter” to that of a “higher-value and more stable exporter.”