Gemini Cooperation Reallocates Vessel Capacity Toward the Mediterranean: How Are Global Shipping Alliances Adapting?

02/07/2026

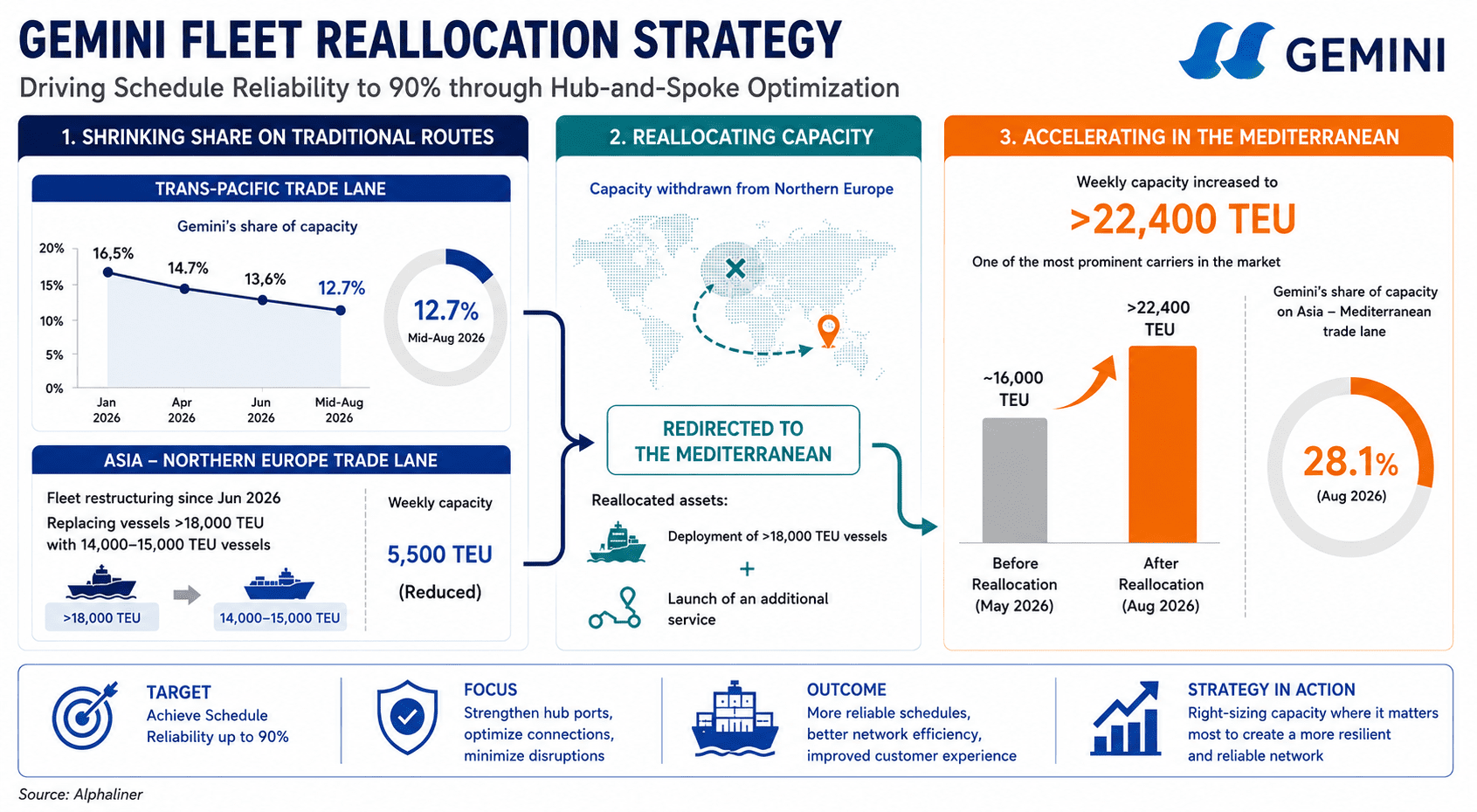

The global carrier alliance landscape is undergoing a massive, calculated restructuring. While high-level market share data initially suggested that the newly minted Gemini Cooperation (Maersk and Hapag-Lloyd) was simply losing ground across major East-West corridors, a deeper volume variance analysis reveals a deliberate, aggressive network redesign. Gemini is actively sacrificing capacity market share on the Transpacific and Asia-North Europe trade lanes to fund an all-out offensive aimed at dominating the Asia-Mediterranean trade lane.

To back their ambitious 90% schedule reliability target, Gemini has shifted heavily toward a dense hub-and-spoke model. The physical execution of this network strategy has resulted in a stark bifurcation:

- The Strategic Retreat: On the Transpacific route, Gemini's capacity market share has steadily eroded, dropping to 12.7% by mid-August 2026. Similarly, on the Asia-North Europe lane, Gemini executed a sharp structural fleet downgrade in June 2026, pulling its massive 18,000+ TEU vessels and replacing them with smaller 14,000 to 15,000 TEU ships—effectively cutting its weekly European capacity by roughly 5,500 TEUs.

- The Mediterranean Offensive: The tonnage pulled from Northern Europe didn't exit the water; it cascaded directly into the Mediterranean. Backed by these 18,000+ TEU vessels and the launch of a brand-new fourth service loop, Gemini’s absolute net capacity injection into the Mediterranean skyrocketed by over 22,400 TEUs weekly, driving their market share to a dominant 28.1%.

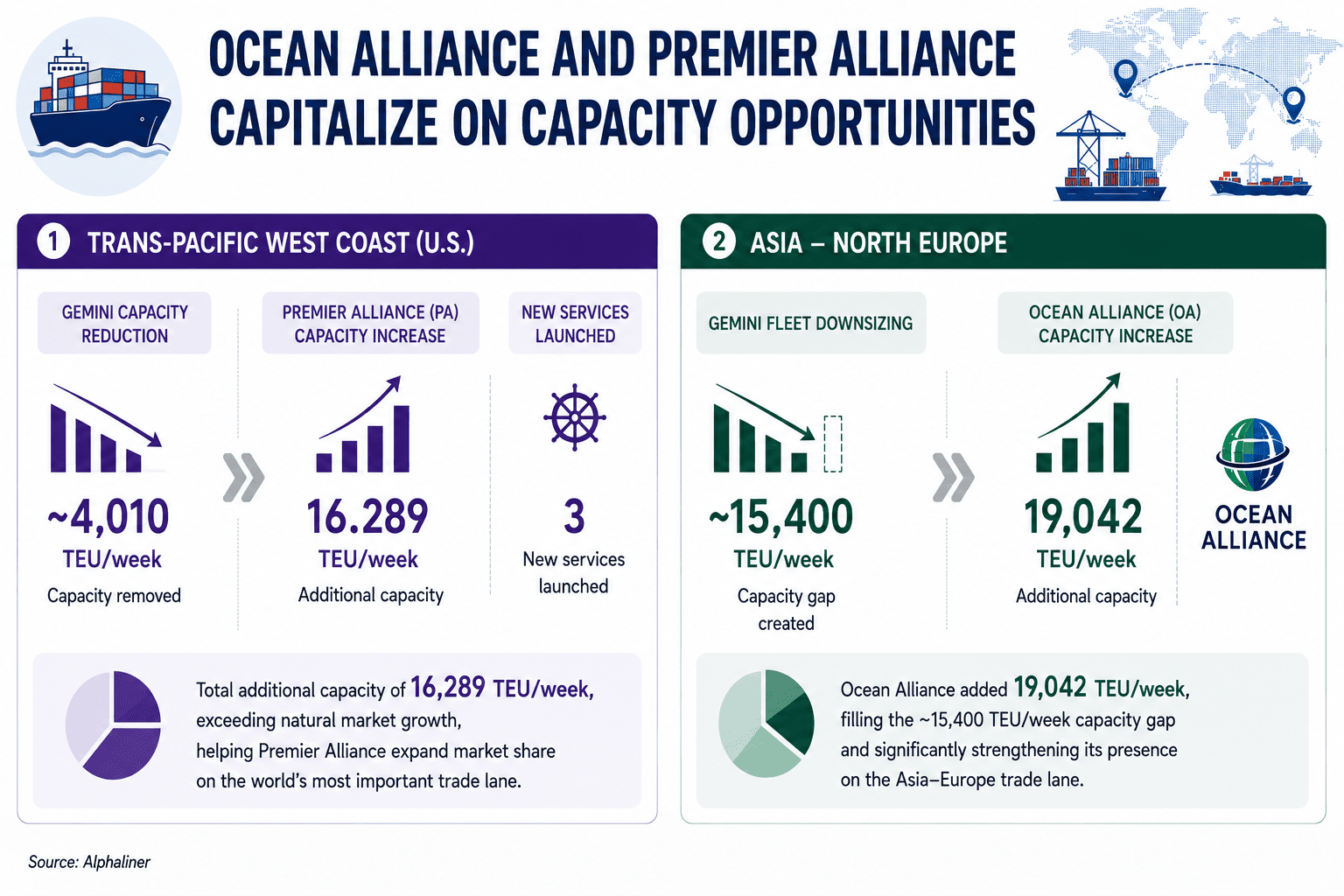

The Primary Beneficiaries: Ocean Alliance and Premier Alliance

Gemini’s willingness to step back has left massive market vacuums, and competing alliances are aggressively capturing the fallout:

- On the Transpacific West Coast: Gemini’s pullback removed 4,010 TEUs of weekly capacity. The primary beneficiary was Premier Alliance (PA), which launched three net new services, injecting an extra 16,289 TEUs weekly and significantly outlashing the trade lane's baseline growth.

- On the Asia-North Europe Lane: Gemini’s downsizing generated a negative market share effect of nearly 15,400 TEU per week. Ocean Alliance (OA) capitalised instantly, overshooting market growth by dumping an astonishing 19,042 TEUs of fresh weekly capacity onto the lane.

Secondary Corridors: The Rise of Alternative Markets

This alliance maneuvering is happening against a backdrop of surging secondary markets, particularly in Africa and Latin America, which are currently yielding highly lucrative freight rates. For instance, MSC has severely pulled back its Mediterranean presence to aggressively redeploy its assets into these high-growth corridors, launching dedicated intra-regional services like the "Dar Es Salaam Shuttle" to connect rising trade hubs in Kenya and Tanzania.

For regional supply chains, these alliance shifts mean that container space, vessel sizes, and routing frequencies are no longer uniform. Shippers must align with the specific alliances expanding capacity on their target trades to secure stable allocations.

Why Vietnam Is Benefiting from Alliance Capacity Shifts

The redistribution of capacity among the major carrier alliances is particularly relevant for Vietnam because the Cai Mep – Thi Vai deep-water port complex has become one of the most important transshipment and gateway hubs in Southeast Asia.

As Ocean Alliance and Premier Alliance expand their presence on key East–West trade lanes, additional vessel deployments inevitably require reliable hub ports capable of handling ultra-large container vessels (ULCVs) and supporting dense feeder networks. Cai Mep – Thi Vai is well positioned to capture this growth thanks to its deep-water infrastructure, direct connections to major global markets, and growing role within alliance service networks.

In practical terms, Gemini's capacity withdrawal does not necessarily translate into lower volumes for Vietnam. Instead, the market share captured by competing alliances may generate additional vessel calls and cargo throughput at terminals serving Ocean Alliance and Premier Alliance networks. This helps explain why several terminals within the Cai Mep – Thi Vai complex continue to record strong growth despite the ongoing restructuring of global alliance networks.

Market Outlook

The structural shifting of weekly capacity by Ocean Alliance (+19,042 TEUs) and Premier Alliance (+16,289 TEUs) directly impacts the Cai Mep - Thi Vai (CMTV) deep-water complex, driving an influx of multi-alliance mega-vessels. As the global logistics industry witnesses alliances shifting tonnage to secondary corridors like Africa, Vietnamese port networks must expand their feeder connections to accommodate more diverse, non-traditional trade lanes feeding into these mainlines.