Vietnam's Rice Supply Chain and Exports: Logistics "Bottlenecks" and the Cost Challenge

07/05/2026

The Transformation of the "Pearl of Heaven"amidst the 2025-2026 Global Macroeconomic Context

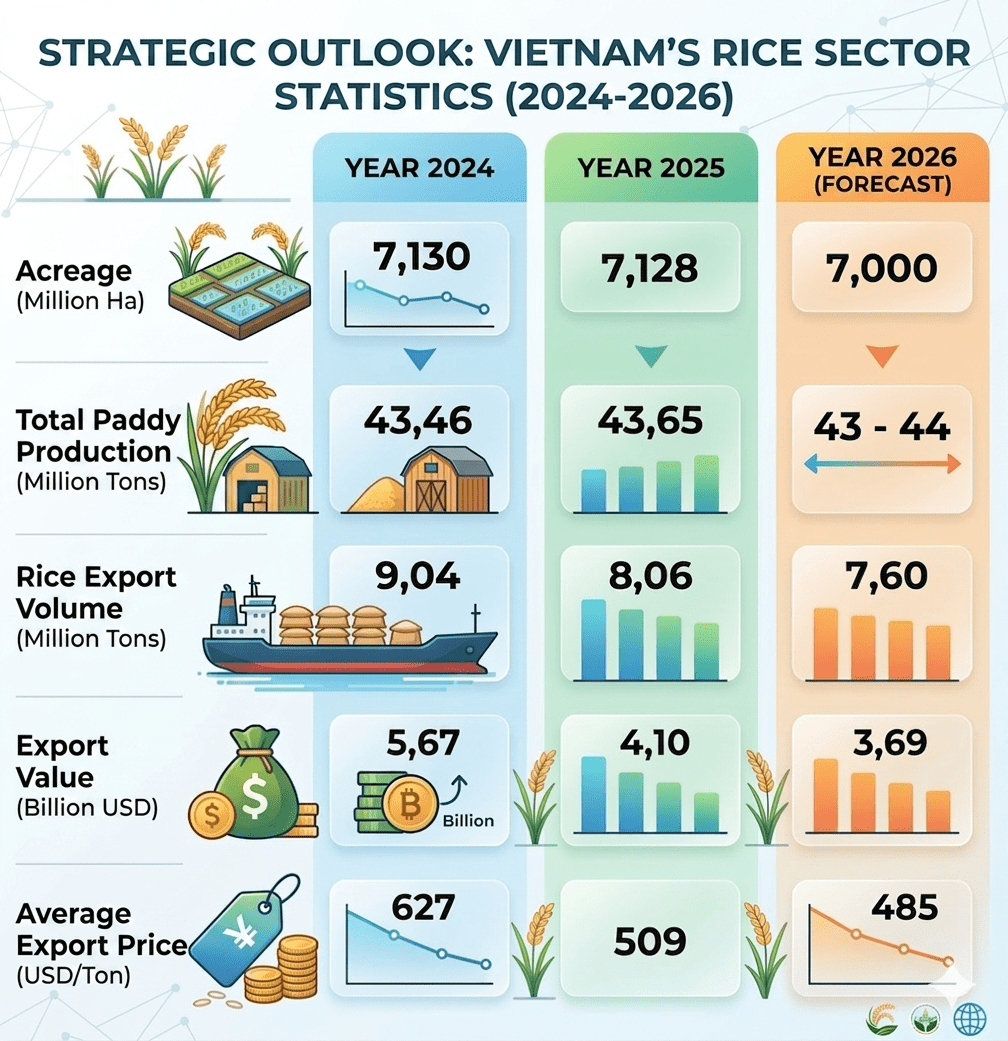

On one hand, Vietnam continues to maintain impressive production capacity with an annual yield fluctuating around 43 to 44 million tons of paddy, with the Mekong Delta region contributing over 50% of the output and 90% of the export volume. On the other hand, the recovery of supply from major competitors and geopolitical disruptions at vital maritime chokepoints are forcing a comprehensive reevaluation of our cost structure and supply chain operating model.

Trong During this period, the rice industry is no longer merely a story of productivity or cultivated area. Although the area tends to decrease slightly to 7.0 - 7.09 million hectares in 2026 due to urbanization and crop conversion, the average yield shows significant improvement, projected to reach 6.21 tons/ha thanks to the penetration of advanced seed technology and farming techniques.

This is a testament to the shift from horizontal to vertical development, prioritizing value over pure volume.

However, this transition is taking place in a "multipolar" global supply environment, where national food policies from India or Thailand can upend price forecasts within mere weeks.

Import-Export Realities: When Numbers Reflect Competitive Pressures

As of the end of April 2026, Vietnam exported approximately 3.3 million tons of rice, generating a turnover of 1.57 billion USD. Compared to the same period in 2025, the volume only slightly decreased by 2.3%, but the value dropped by 11.1%.

This reflects a harsh reality: the average export price of rice dropped to 468.4 USD/ton, a decrease of about 9% year-on-year.

Notably, the Philippines maintains its position as Vietnam's largest import market, accounting for approximately 42.5% of total rice exports in Q1 2026. However, this nation is also diversifying its supply sources and implementing flexible tariff mechanisms, exerting considerable pressure on the profit margins of Vietnamese enterprises.

The structure of export rice varieties is also undergoing crucial transformations to adapt to new market requirements. Fragrant rice and high-quality rice such as DT8 and OM18 hold an overwhelming proportion, reaching nearly 49% of total exports. Meanwhile, standard white rice varieties face fierce competition from Pakistan and Myanmar – countries with an inherent advantage in lower production costs within the popular rice segment.

Rủi ro kép tác động đến xuất khẩu gạo Việt Nam

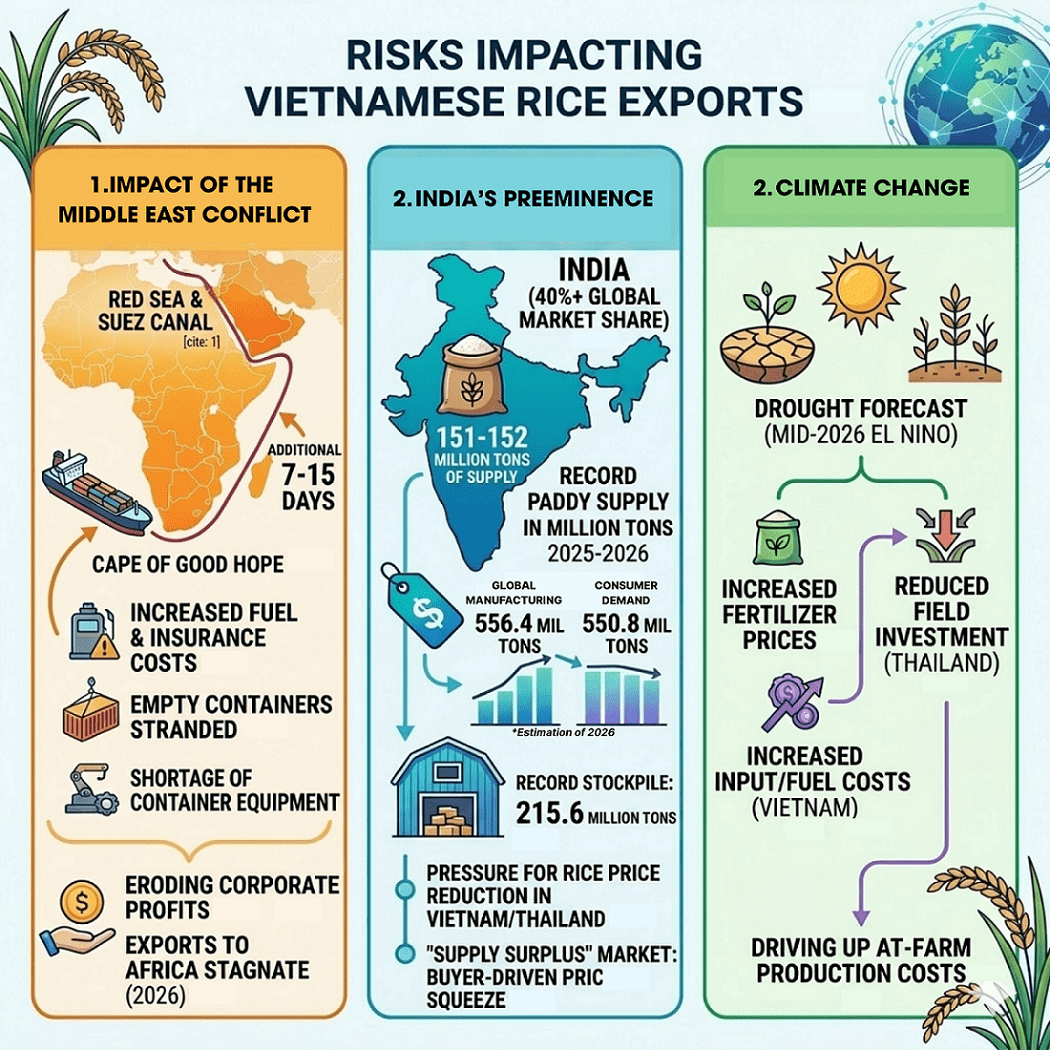

Impact of the Red Sea Conflict and Global Supply Chain Risks

The conflict in the Middle East has paralyzed the shipping route through the Red Sea and the Suez Canal, traditionally the shortest path connecting Vietnamese rice to potential markets in Europe and North Africa. Shipping lines have been forced to opt for the safer alternative of routing via the Cape of Good Hope, extending transit times by 7 to 15 days. This prolonged duration not only escalates bunker costs but also triggers a domino effect: empty containers are stranded on vessels taking the longer detour, leading to a severe shortage of loading equipment at ports of origin.

Consequently, ocean freight rates and cargo insurance premiums have skyrocketed. For agricultural commodities with low unit value and razor-thin margins like rice, any incremental surge in logistics costs directly erodes corporate profitability. In many instances, enterprises are compelled to adjust delivery schedules or accept high commercial risks to honor contracts. This explains why, despite significant demand from the African market, Vietnam's rice exports to this region tend to stall in 2026.

India's Dominance and the New Rice Pricing Order

Following a period of restrictive measures, India has aggressively re-entered the market with a projected record supply of 151 - 152 million tons of paddy in the 2025 - 2026 crop year. Armed with massive accumulated inventories, India currently acts as the global market's "price anchor." When this nation, which holds over 40% of the global rice market share, offloads its stockpiles, downward pressure on Vietnamese and Thai rice prices is inevitable.

Furthermore, global production is projected to surge to 556.4 million tons in the upcoming crop year, far exceeding the estimated consumption demand of 550.8 million tons, driving ending inventories to a record high of 215.6 million tons. This state of "oversupply" is shifting the market from a seller's to a buyer's position, where importing nations possess the leverage to be selective and aggressively negotiate lower prices.

Climate Change and the Input Cost Conundrum

One cannot overlook the impact of El Niño, a phenomenon forecasted to cause severe droughts in Southeast Asia from mid-2026. In rival nations like Thailand, farmers face substantial fertilizer price hikes, forcing them to cut back on field investments, thereby threatening yields. Although Vietnam benefits from a more proactive irrigation system, it is not immune to the inflationary spiral of agricultural inputs and machinery operational fuel. This indirectly inflates farm-gate production costs while global selling prices exhibit a downward trajectory.

Logistics Bottlenecks of Vietnam's Rice Value Chain

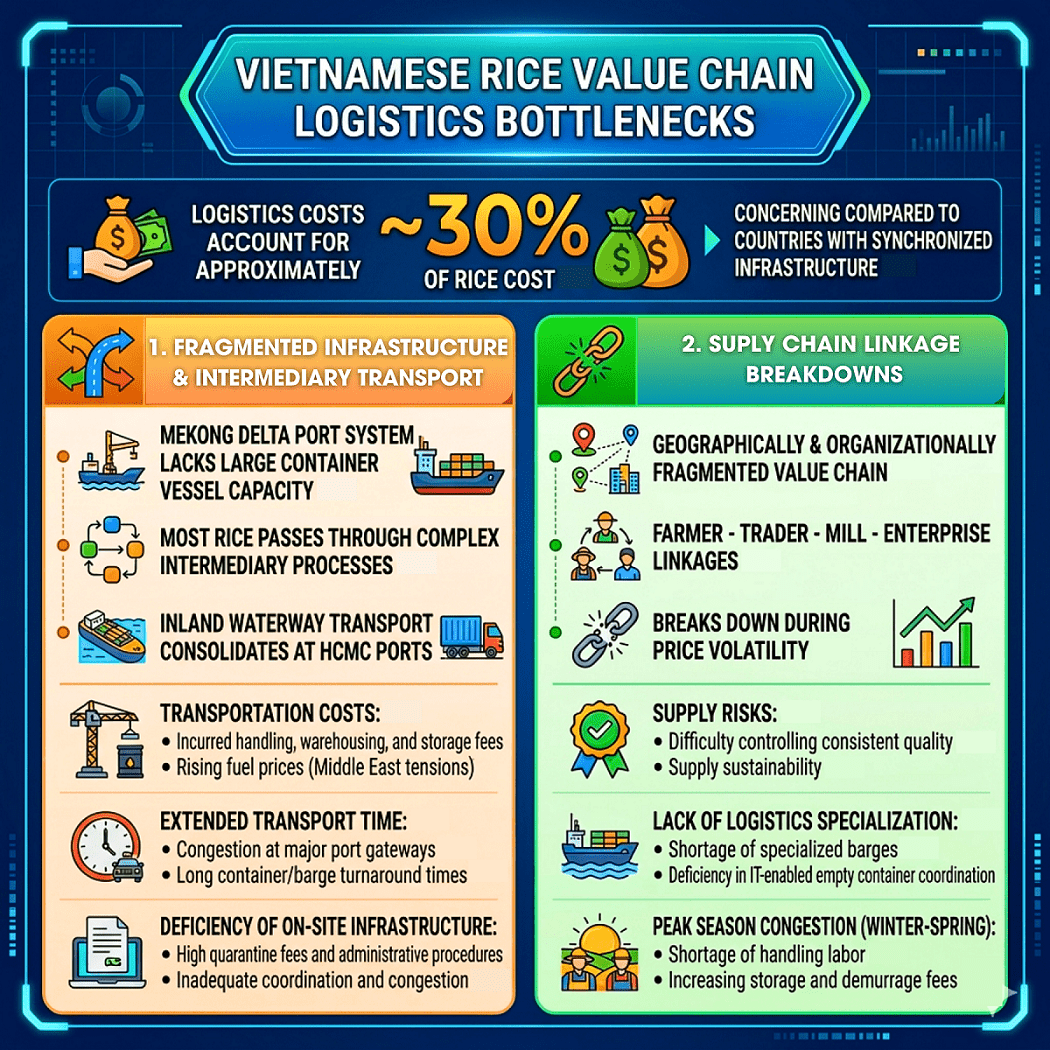

Currently, logistics costs account for approximately 30% of the product cost of rice. This is an absurd figure when compared to countries with synchronized infrastructure.

Fragmented Infrastructure and Reliance on Intermediary Transport

The Mekong Delta is the nation's rice bowl, yet its seaport system lacks the capacity to accommodate large-tonnage container vessels. The majority of export rice must traverse a complex intermediary transport process: from small boats and barges at the fields or milling plants, navigating through silted inland waterways to aggregate at major ports in Ho Chi Minh City.

This process incurs a multitude of unnecessary costs:

2. Prolonged Transit Times: Delays caused by tides and congestion at major port gateways extend the turnaround time of containers and barges, inflating operational costs for enterprises.

3. Localized Infrastructure Deficits: Inspection/quarantine, warehousing, and administrative procedure costs remain high; coordination work is still inadequate, making congestion likely to occur.

Fractures in the Supply Chain Linkage

The current rice value chain remains fragmented both geographically and organizationally. The linkage among Farmers - Traders - Milling Plants - Export Enterprises frequently breaks down amidst price volatility. Heavy reliance on the trader (middleman) system makes it challenging for exporters to control uniform quality and the sustainability of supply.

The logistics system serving the rice industry also lacks specialization. The lack of dedicated barge fleets and the application of information technology to efficiently coordinate empty containers. During the peak Winter-Spring harvest season, port congestion and shortages of stevedoring labor are frequent occurrences, reducing operational efficiency and inflating demurrage and storage costs.

Market Orientation and 2026 Action Strategy to The long term vision

Key Production and Export Objectives

In 2026, Vietnam aims to maintain paddy production at 43 to 44 million tons to ensure national food security and cater to exports. Export rice volume is projected to remain stable between 7.5 and 7.7 million tons. A noteworthy point in this strategy is the robust shift in product structure: continuing to increase the proportion of fragrant rice, specialty rice, and high-quality rice, while proactively phasing out low-grade rice to elevate the brand image of Vietnamese rice on the global map.

Market Strategy: Securing Tradition, Expanding Potential

Vietnam is determined to maintain a solid presence in traditional markets such as the Philippines (currently holding over 40% market share), China, Malaysia, and West African nations like Ghana and Ivory Coast. However, faced with policy fluctuations from importing countries, the new direction is to intensify expansion into other potential regions, including the remaining African countries, North Asia, and the Americas. In particular, boosting exports through Government-to-Government (G2G) contracts will serve as a "shield" to stabilize outlets against the unpredictable vagaries of the free market.

Challenges in the New Orientation

his roadmap is not without its hurdles. Prolonged natural disasters and floods could reduce cultivated areas, while complex paddy price dynamics might discourage farmers, prompting them to switch to alternative crops. Furthermore, the food autonomy policies of major importers like Indonesia and Malaysia will render the market more fiercely competitive than ever.

To actualize these orientations, coordination between the State Agencies and Enterprises is a necessary condition.

2. Maximize FTA Utilization: Fully exploit tariff preferences from the EVFTA and CPTPP to alleviate cost burdens and penetrate premium segments

3. Strategic Logistics Partnerships: Instead of short-term spot contracts, businesses should sign long-term agreements with reputable shipping lines and freight forwarders to stabilize freight rates and secure container equipment.

4. Số hóa và tối ưu hóa vận hành: Apply IoT and Blockchain technology for end-to-end quality monitoring and to optimize stowage plans, thereby reducing vessel waiting times at ports.

The Constructive Role of the State

The State must accelerate logistics infrastructure investments in the Mekong Delta, especially deep-water ports like Tran De, to relieve pressure on the existing port system. Simultaneously, measures are needed to stabilize transport costs and support the resolution of difficulties arising during the execution of large rice export contracts.

The Vietnamese rice sector in the 2025 - 2026 phase resides in a "state of structural volatility." We cannot expect to return to the era of record-high prices without systemic transformations.

The challenge from India, risks from the Red Sea, or domestic logistics bottlenecks are merely litmus tests for us to realize that the sole path to sustainable development is transitioning from a volume-centric mindset to a value-centric one, underpinned by a green and smart supply chain.

The resolute implementation of the 1-Million-Hectare High-Quality Rice Project, coupled with clear market orientations from the VFA and efforts to modernize logistics infrastructure, will serve as the launchpad for the "Pearl of Heaven" to truly deliver sustainable prosperity for both farmers and the national economy.

*Soure: “Vietnam’s Rice Supply chain: Logistics Bottlenecks and Cost Challenge” – Vietnam Food Association (VFA)